The Benefits of Including Life Insurance in Your E

Life insurance is a crucial aspect of financial planning that often gets overlooked when it comes to real estate. However, incorporating life insurance into your estate plan can provide numerous benefits, ensuring a smooth and secure legacy for both buyers and homeowners. When thinking about estate

Estate Planning For The Self Employed

Estate Planning For The Self Employed Estate planning is a crucial aspect of financial management, and it becomes even more complex for those who are self-employed. As a self-employed individual, you not only have to consider your personal assets but also take into account the structure of your busi

Categories

- All Blogs (107)

- Advocate (6)

- Appraisals (4)

- Avoiding Probate (1)

- Brokerage (10)

- Buying (48)

- Career (1)

- Closing Insurance (1)

- Commercial (2)

- Commission (2)

- Compensation (1)

- Decor (1)

- Divorce (2)

- Divorce Decree (1)

- Due Diligence (2)

- DYI (1)

- Embracing the Downsizing Journey (4)

- Enhancing Appeal through Upgrades and Staging (2)

- Equity (2)

- Estate Planning (2)

- Exploring Retirement Living Options (1)

- FHA (3)

- Financing & Mortgage Tips (3)

- First Time Buying (15)

- Friendship (2)

- Georgia Real Estate (19)

- Georgia, USA (30)

- Growing (2)

- Hidden Protection (9)

- Highlighting Unique Features (2)

- HOA (3)

- Holiday Events (3)

- Home Inspection (6)

- Home Maintenance (5)

- Homebuyer Education (5)

- Homeowner Protection (17)

- Homeownership (41)

- Insurance (3)

- Land Trust (1)

- Lease Negotiation (2)

- Lender's Title Insurance (1)

- Lending (10)

- Licensed and Insured (1)

- Market (19)

- Marriage (1)

- Mortgage (5)

- Moving (9)

- NAR Settlement (2)

- New Home Journey (13)

- Owner's Title Insurance (1)

- Packing (2)

- Professional Advice (19)

- Property Damage (1)

- Property Taxes (3)

- Quitclaim Deed (1)

- Real Estate (45)

- Real Estate Closing Attorney (5)

- Relocation (12)

- Research and Review (5)

- Retirement Living (1)

- Sales and Acquisitions (4)

- Selling (23)

- Senior Home Solutions (1)

- Senior Housing (1)

- Seniors (2)

- Smart Pricing and Incentives (1)

- Summer (3)

- Title Search (2)

- Transfer Ownership Rights (1)

- VA Home Buying (1)

- VA Loans (1)

Recent Posts

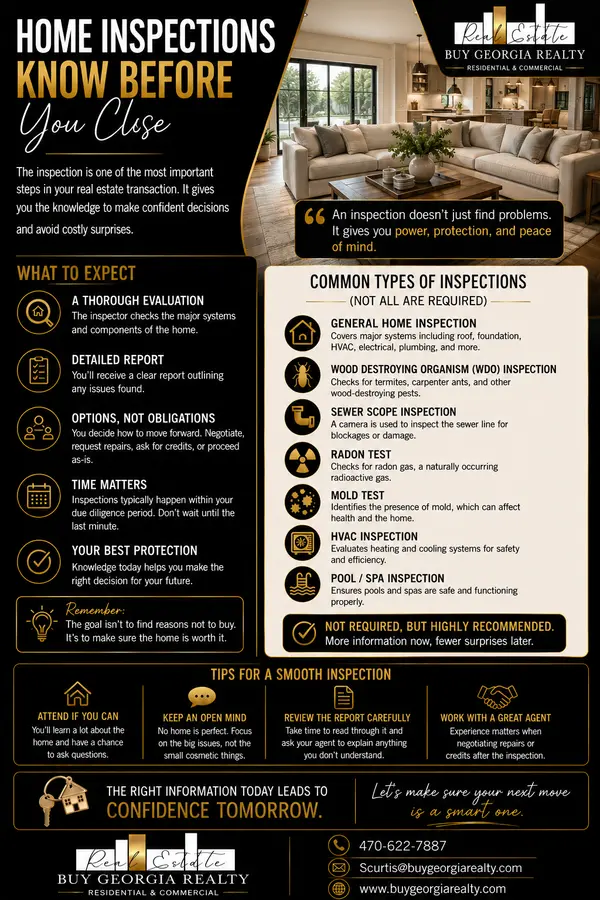

Home Inspections: Know Before You Close

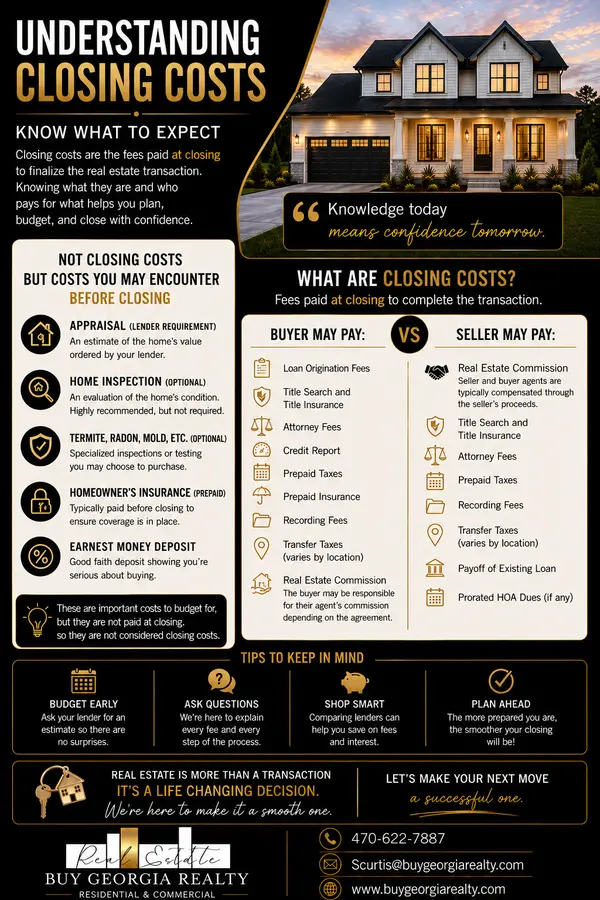

Understanding Closing Costs: Know What to Expect Before You Buy or Sell

Prep Today, Profit Tomorrow: How to Get Your Home Market-Ready Before You List

A Smart Buyer Is an Informed Buyer

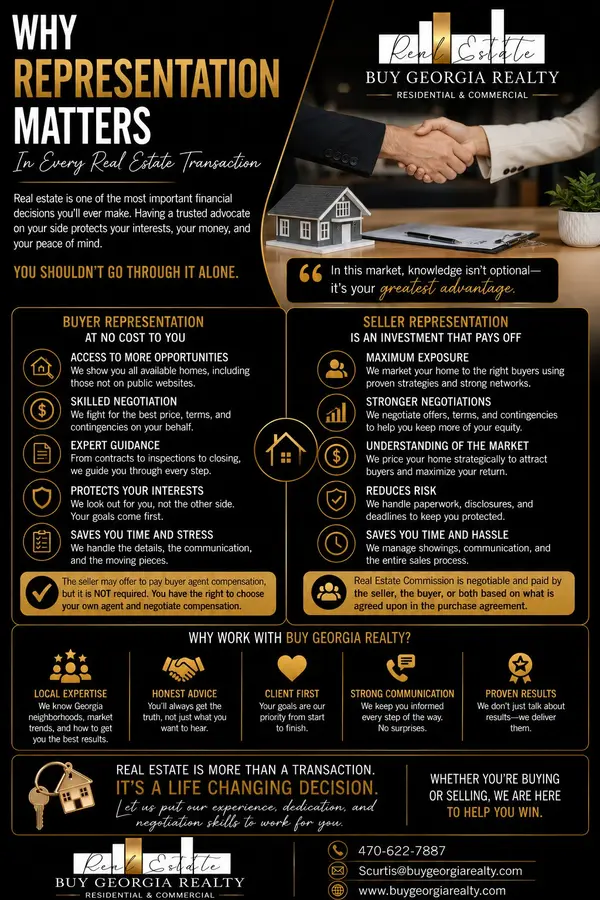

Why Representation Matters in Every Real Estate Transaction

What Home Features Add the Most Value in Georgia?

What Credit Score Do You Need to Buy a Home in Georgia?

Hidden Costs of Buying a Home in Georgia That Most Buyers Don’t Expect

The Due Diligence Period in Georgia: What It Truly Means and Why It Is One of the Most Powerful (and Misunderstood) Parts of a Contract

Are Georgia Home Prices Going to Drop?